Exponential Edge - #6

Rare Metals, XRP Killer & AI L1s

Key Report Insights:

Rare Metal Rotation: Select industrial metals are up 15–20% YTD as investors hedge against fiat risk and supply shocks.

AI x Copper Trade Heating Up: AI’s infrastructure needs are driving an 18% YTD surge in copper.

EV Power Shift to China: U.S. EV dominance is fading as China ramps up demand for copper-heavy vehicles.

Google Vet Backs XRP-Like L1: KTA raised $17M from ex-Google CEO Eric Schmidt, with a $54M market cap and a strong banking narrative.

Gensyn’s Bet on Open-Source AI: A decentralized AI network is live in testnet with 371 models and a TGE on the horizon.

1. Long-Tail Market Overview:

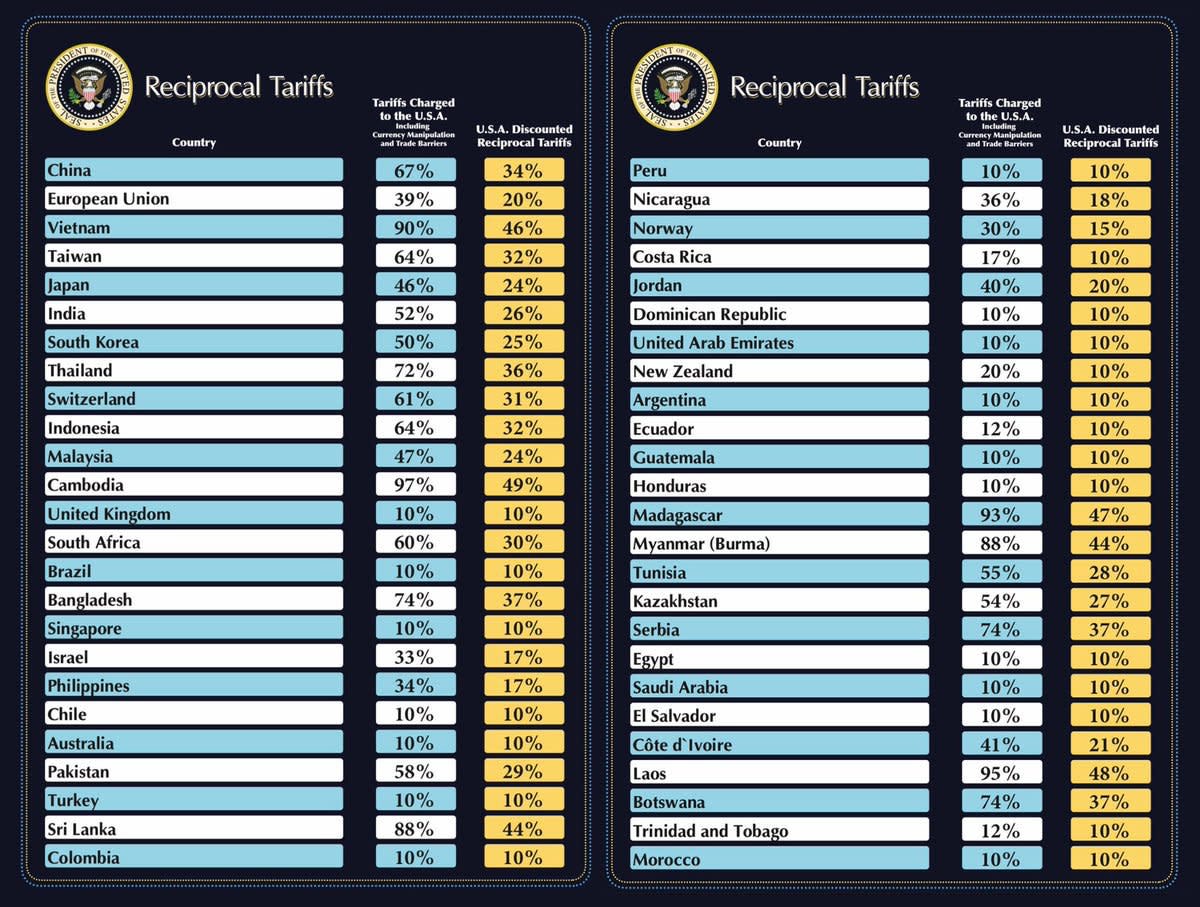

A. Liberation Day Hits Countries:

On April 2, sweeping tariffs of 10–40% were announced for 185 countries.

Southeast Asia—especially Vietnam—was hit hardest, signaling a crackdown on proxy exporters. Expect U.S. domestic manufacturers to benefit.

In response, Eastern markets may attract more capital. The EU is reopening trade talks with China, while China, Japan, and Korea are solidifying regional ties.

Polymarket offers a real-time macro read—odds of a 2025 U.S. recession jumped to 57% post-'Liberation Day.'

Source: Yahoo Finance

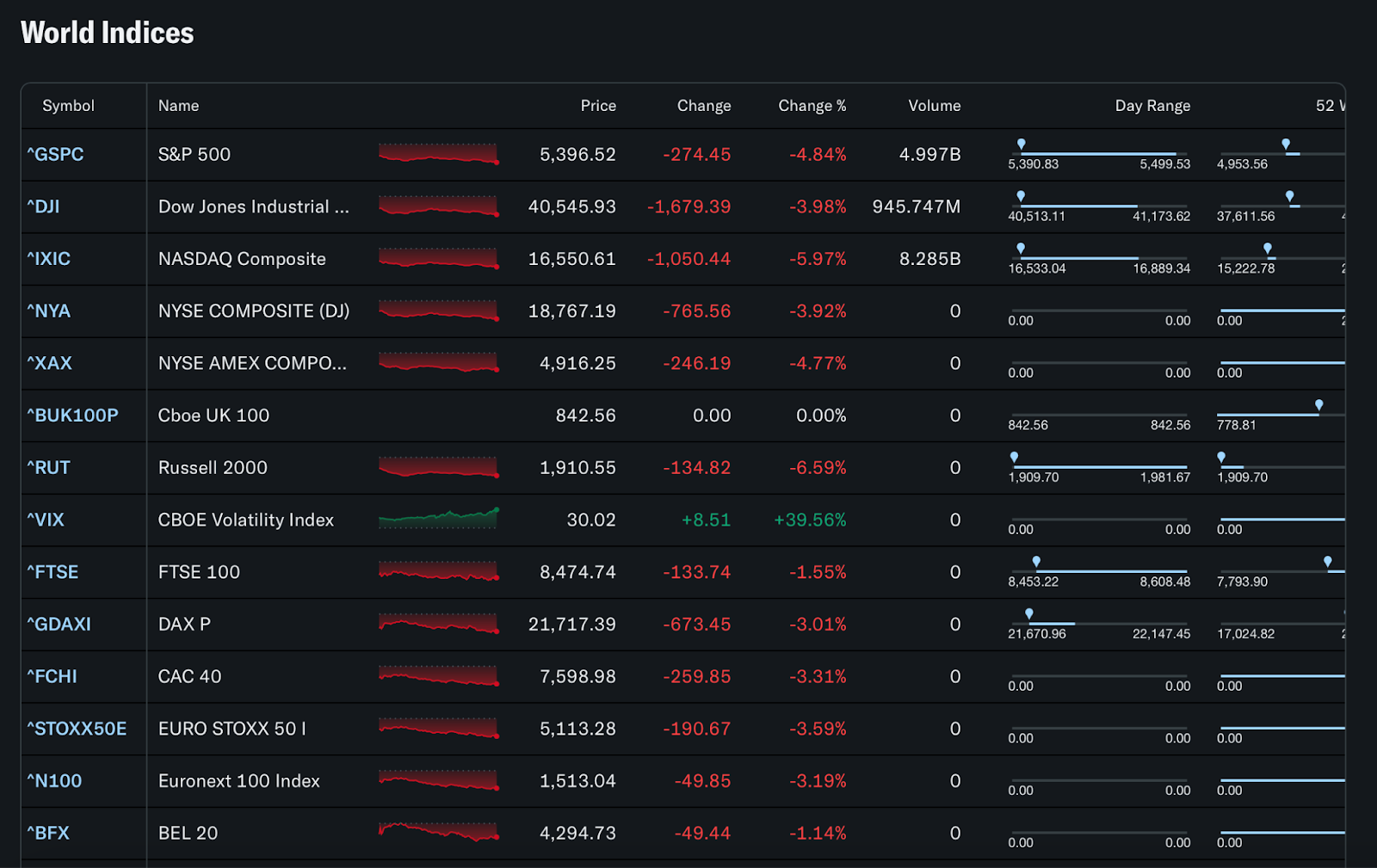

B. Risk Asset Performance Post April 2:

Markets sold off globally following the tariff shock, with indices sliding as traders priced in the hit to global trade.

Consumers face rising prices as import costs get passed down, squeezing demand—especially in the consumer goods sector, where earnings projections are already falling.

Tech stocks were hit hardest. In a risk-off world, growth premiums shrink fast—challenging the lofty valuations that once propped them up.

Source: Yahoo Finance

C. BTC’s Strength Amidst The Chaos:

Since the April 2 tariffs, BTC has outpaced the S&P 500 by ~13%, as investors rotate into hard assets and the dollar softens.

If the Fed responds with rate cuts and liquidity injections, BTC remains the fastest horse—closely tied to global liquidity flows.

But it’s not a one-way trade. Prolonged trade weakness could suppress global liquidity, dragging BTC down too.

MVRV Z-Score sits at 1.77—well below euphoric bull tops (~7)—suggesting room to run, but not without risk.

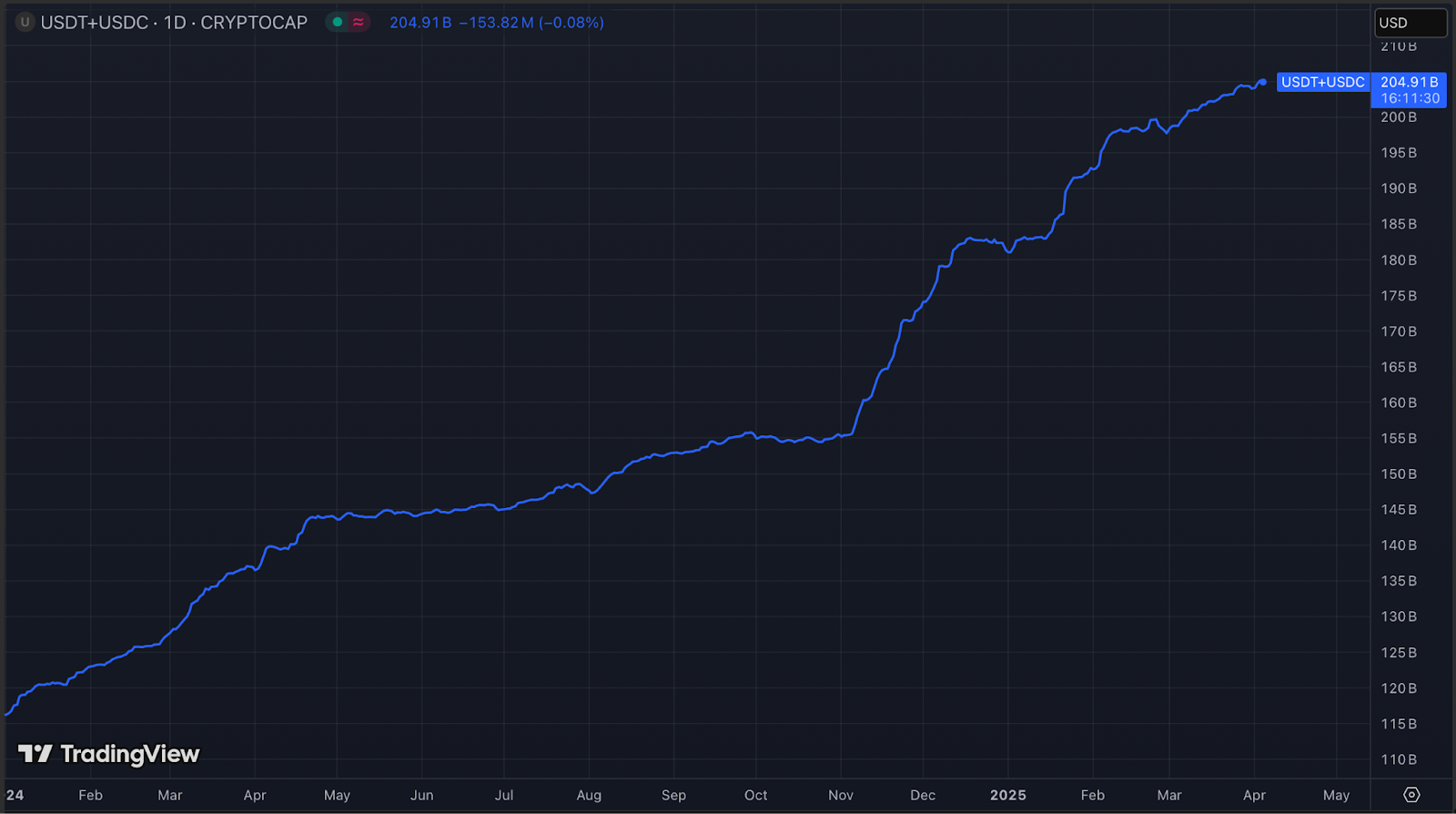

D. Circle’s IPO: The First Pure Stablecoin Play

Circle, issuer of USDC, has officially filed for an IPO—marking the first major public bet on stablecoin adoption.

Stablecoins are gaining traction in TradFi as tokenization accelerates, offering a new payments backbone with real-world utility.

Amid crypto’s volatility, stablecoins offer a steady, TradFi-friendly business model. The GENIUS Act further legitimizes the space, easing regulatory concerns.

With Tether remaining private, Circle becomes the go-to proxy for stablecoin growth—and possibly a gateway stock for broader blockchain exposure.

E. OpenAI Secures $40B Funding:

OpenAI just secured $40B from Softbank, pushing its valuation to $300B—miles ahead of Anthropic’s $61.5B.

The funding arms OpenAI to crush rivals like DeepSeek and BABA, but profitability is still distant.

Revenues may triple to $12.7B by 2025, yet sky-high compute and talent costs keep margins thin.

Its profit path hinges on two levers: more businesses using its API and model subscriptions.

Want exposure? Microsoft remains a strong proxy, earning a slice of OpenAI’s revenue stream.

Source: OpenAI

The author(s) own BTC at the time of writing (disclaimer).

| A guest post by

|