Software isn’t collapsing — it’s undergoing a forced repricing. IGV is down 17% YTD vs QQQ as AI disruption drives a heavy rotation.

This dislocation is creating asymmetric setups among mispriced software survivors, which we outline in this report.

We also highlight emerging energy opportunities and a hidden Western-listed proxy for ByteDance’s AI-driven growth in China.

Stay through to the end for key public portfolio updates — now up +23.5% vs QQQ since July 2025.

Key Report Insights:

AI Repricing Shock: Software de-rating opens selective alpha

Earnings Reality: 79% SPX beats reinforce profit-driven bid

Policy Torque: $12B uranium stockpile shifts supply dynamics

Vertical Integration: CCJ captures fuel → reactor value chain

CapEx Supercycle: China + Western hyperscaler spending drives AI infra

1. Market Overview:

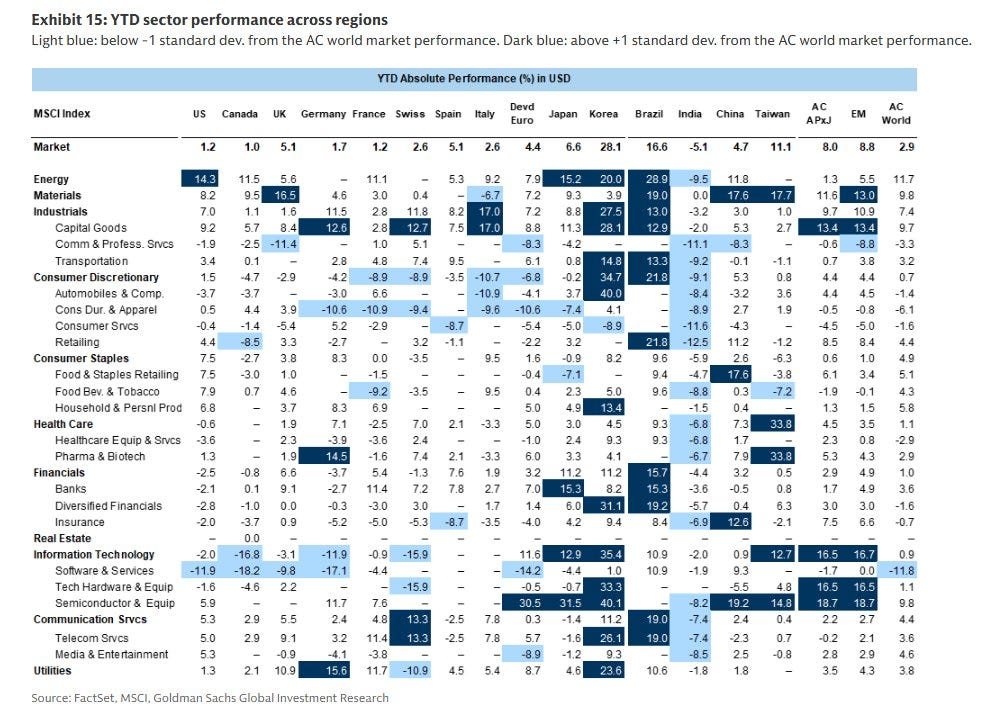

A. The Emerging Market Leaders:

Emerging markets are gaining momentum into 2026, outperforming developed peers as commodity scarcity and earnings inflection drive returns.

YTD leaders include South Korea — powered by semiconductor and memory strength — and Brazil, led by energy and base metals.

Source: Mike Zaccardi on X

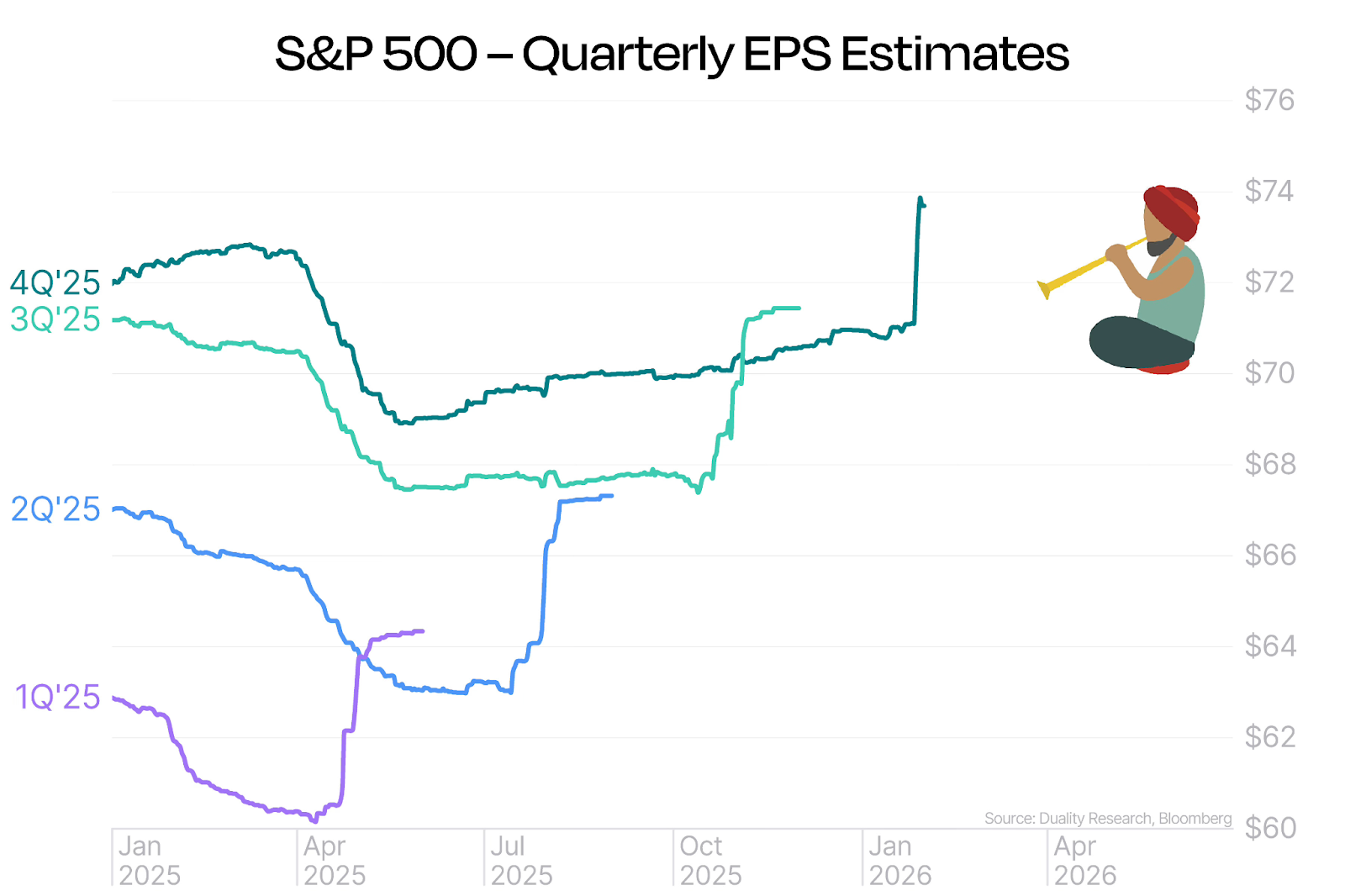

B. It’s Earnings Season:

Despite elevated volatility, the S&P 500 remains positive (+1.91% YTD) as earnings season gains momentum.

So far, 79% of companies have beaten estimates — reinforcing the rally with tangible profit strength rather than sentiment alone.

Source: Duality Research

2. Software:

A. The Software Reversion:

Software has underperformed QQQ over the past year and is down another 17% YTD as AI pressures market share and compresses margins.

Tools like Claude Code are commoditizing coding, enabling non-technical users to build without deep expertise.

Despite valid concerns, depressed valuations may create mean-reversion opportunities among companies still delivering solid growth.

B. Long Expertise, Short Enterprise:

Catching a software bottom is high risk; a long/short approach offers better risk-adjusted exposure.

Long: ADBE — GenAI acts as a complement to its creator ecosystem, positioning AI as an upgrade rather than a replacement. Growth remains intact: Q4 2025 revenue hit a record $6.19B (+10% YoY), FY2025 cash flow exceeded $10B, and forward P/E sits at 11.55.

This post is for paid subscribers

| A guest post by

|